All Categories

Featured

Table of Contents

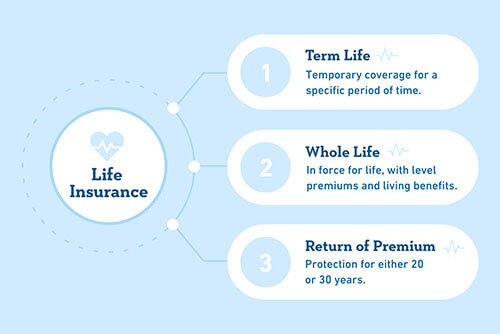

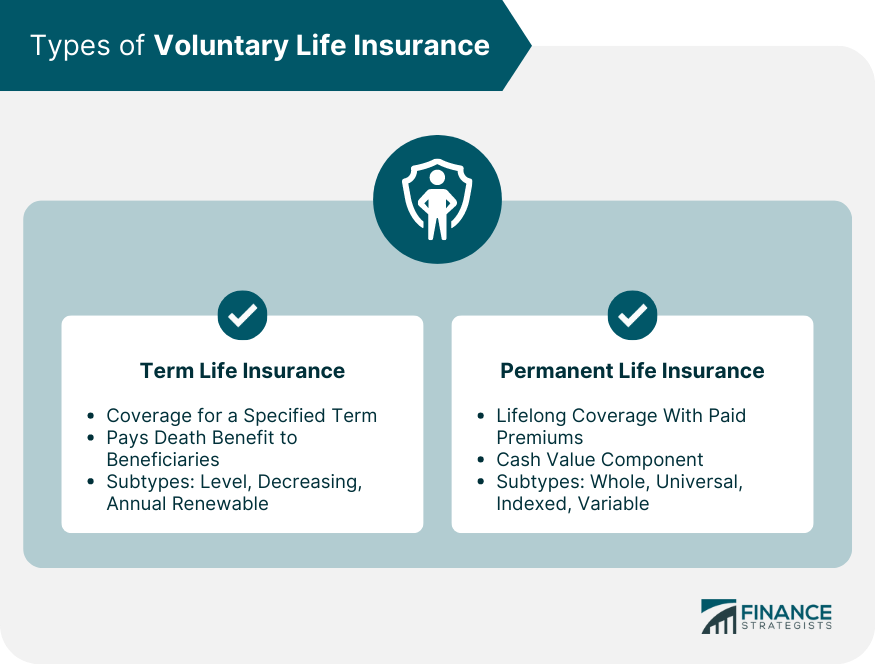

Term Life Insurance Policy is a sort of life insurance coverage plan that covers the insurance policy holder for a certain quantity of time, which is understood as the term. The term lengths differ according to what the individual selects. Terms usually vary from 10 to thirty years and rise in 5-year increments, offering level term insurance coverage.

They normally provide an amount of insurance coverage for a lot less than irreversible kinds of life insurance policy. Like any type of plan, term life insurance policy has advantages and downsides relying on what will function best for you. The advantages of term life consist of affordability and the ability to personalize your term size and coverage amount based upon your requirements.

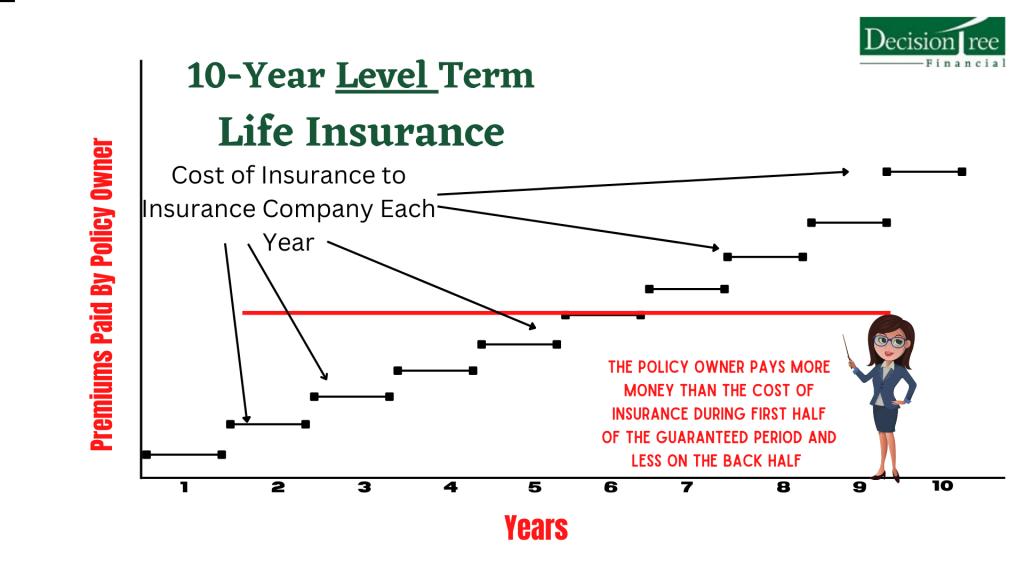

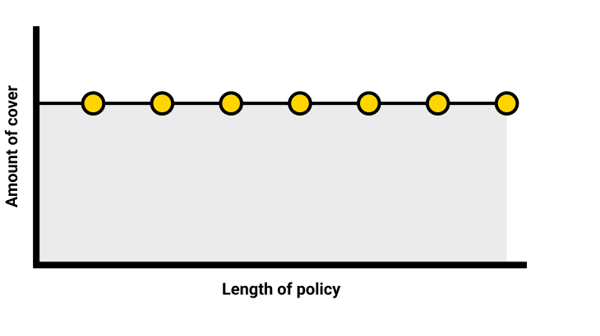

Depending on the type of policy, term life can supply fixed costs for the whole term or life insurance coverage on level terms. The death advantages can be taken care of.

You should consult your tax advisors for your details accurate scenario. *** Rates mirror plans in the Preferred Plus Rate Course issues by American General 5 Stars My agent was very educated and helpful while doing so. No stress to buy and the procedure fasted. July 13, 2023 5 Stars I was pleased that all my requirements were fulfilled without delay and properly by all the reps I talked with.

What is Voluntary Term Life Insurance? Explained in Detail

All documentation was digitally completed with access to downloading for individual file maintenance. June 19, 2023 The endorsements/testimonials provided should not be taken as a recommendation to buy, or a sign of the value of any kind of services or product. The reviews are real Corebridge Direct clients who are not associated with Corebridge Direct and were not provided settlement.

There are several sorts of term life insurance policy plans. As opposed to covering you for your whole lifespan like entire life or global life plans, term life insurance policy just covers you for a marked time period. Policy terms generally vary from 10 to 30 years, although shorter and longer terms might be readily available.

Many commonly, the policy runs out. If you wish to maintain protection, a life insurer might offer you the alternative to renew the policy for one more term. Or, your insurance company might permit you to transform your term plan to a permanent policy. If you added a return of costs rider to your policy, you would obtain some or every one of the money you paid in premiums if you have actually outlasted your term.

Degree term life insurance coverage may be the most effective alternative for those who want coverage for a collection duration of time and want their premiums to remain steady over the term. This may relate to buyers worried about the affordability of life insurance policy and those that do not intend to alter their survivor benefit.

That is due to the fact that term plans are not assured to pay, while long-term plans are, provided all costs are paid. Degree term life insurance policy is typically a lot more costly than decreasing term life insurance, where the survivor benefit lowers gradually. Other than the type of plan you have, there are several various other variables that assist determine the price of life insurance policy: Older applicants typically have a greater mortality risk, so they are normally more expensive to insure.

On the other side, you might be able to protect a less expensive life insurance policy rate if you open up the plan when you're younger. Comparable to advanced age, poor wellness can also make you a riskier (and a lot more pricey) candidate forever insurance. However, if the condition is well-managed, you may still have the ability to find inexpensive protection.

What is 30-year Level Term Life Insurance? How to Choose the Right Policy?

Health and age are typically much more impactful premium factors than gender. Risky pastimes, like diving and skydiving, may lead you to pay even more forever insurance coverage. Likewise, high-risk work, like home window cleaning or tree cutting, may also drive up your cost of life insurance policy. The finest life insurance policy business and policy will rely on the individual looking, their individual score variables and what they require from their policy.

The primary step is to identify what you need the policy for and what your budget is. As soon as you have a great idea of what you want, you may want to contrast quotes and policy offerings from several companies. Some business supply online quoting permanently insurance, yet lots of need you to contact an agent over the phone or personally.

1Term life insurance policy supplies momentary security for a vital period of time and is usually less costly than irreversible life insurance policy. 2Term conversion guidelines and restrictions, such as timing, may use; as an example, there might be a ten-year conversion benefit for some products and a five-year conversion opportunity for others.

3Rider Insured's Paid-Up Insurance Purchase Choice in New York. 4Not available in every state. There is a cost to exercise this biker. Products and riders are available in approved jurisdictions and names and attributes may differ. 5Dividends are not ensured. Not all participating plan proprietors are qualified for rewards. For select riders, the condition relates to the guaranteed.

Our term life options include 10, 15, 20, 25, 30, 35, and 40-year policies. One of the most preferred type is level term, suggesting your settlement (premium) and payment (death benefit) stays level, or the same, until the end of the term duration. 20-year level term life insurance. This is one of the most uncomplicated of life insurance policy alternatives and requires extremely little maintenance for policy proprietors

As an example, you might give 50% to your partner and divided the rest among your grownup kids, a moms and dad, a good friend, or also a charity. * In some instances the survivor benefit may not be tax-free, discover when life insurance coverage is taxable.

Is What Is Direct Term Life Insurance Right for You?

There is no payout if the plan expires before your death or you live beyond the policy term. You may be able to restore a term policy at expiration, however the premiums will be recalculated based on your age at the time of revival.

At age 50, the premium would increase to $67 a month. Term Life Insurance Rates 30 years old $18 $15 40 years old $28 $23 50 years old $67 $51 Source: Quotacy. Quotes are for a $250,000 30-year term life policy, for males and ladies in outstanding health.

The reduced danger is one element that allows insurance firms to charge lower premiums. Rate of interest prices, the financials of the insurance coverage business, and state regulations can likewise impact premiums. Generally, firms typically use better rates at the "breakpoint" protection levels of $100,000, $250,000, $500,000, and $1,000,000. When you think about the amount of protection you can get for your costs bucks, term life insurance policy tends to be the least costly life insurance coverage.

{kind=link}

Latest Posts

Funeral Expense Plans

Final Expense Life Insurance Jobs

Burial Insurance State Farm