All Categories

Featured

Table of Contents

Life insurance representatives sell mortgage protection and loan providers offer mortgage defense insurance, at some point. mortgage protection insurance pre existing medical conditions. Below are the 2 types of representatives that sell mortgage protection (term life insurance for mortgage protection).

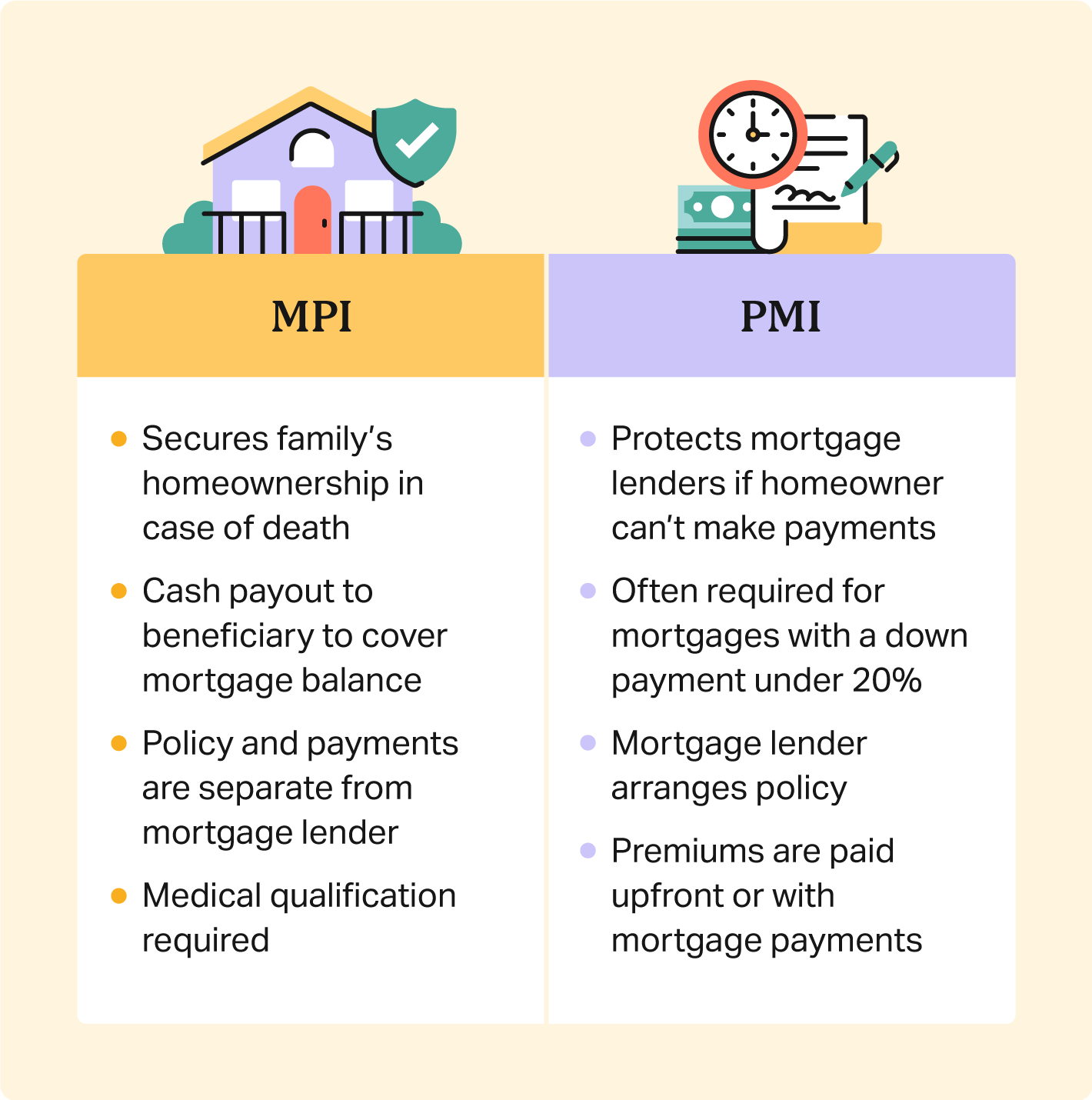

Getting home loan defense through your lender is not constantly a very easy task, and most of the times fairly confusing. But, it is possible. Lenders usually do not sell mortgage defense that benefits you. mortgage interest rate insurance. This is where things obtain puzzling. Lenders sell PMI insurance policy which is developed to secure the loan provider and not you or your family.

Mortgage Protection Plan Reviews

The letters you get appear to be coming from your loan provider, but they are simply originating from 3rd party companies. loan insurance scheme. If you do not wind up getting traditional home mortgage security insurance coverage, there are other types of insurance coverage you may been needed to have or might wish to take into consideration to safeguard your investment: If you have a mortgage, it will be required

Specifically, you will certainly desire home protection, components protection and personal liability. mortgage insurance mandatory. Additionally, you need to take into consideration adding optional insurance coverage such as flooding insurance policy, quake insurance policy, replacement expense plus, water back-up of sewage system, and various other frameworks insurance for this such as a gazebo, shed or unattached garage. Equally as it appears, fire insurance coverage is a type of home insurance coverage that covers damage and losses triggered by fire

This is the primary choice to MPI insurance coverage. A term plan can be structured for a certain term that pays a lump amount upon your fatality which can be made use of for any objective, consisting of paying off your home mortgage. Entire life is a permanent policy that is extra costly than term insurance policy however lasts throughout your whole life.

Coverage is generally limited to $25,000 or less, but it does secure versus having to tap other funds when an individual dies (mortgage payment protection plan). Final expenditure life insurance coverage can be used to cover medical costs and other end-of-life expenses, consisting of funeral and interment expenses. It is a sort of irreversible life insurance policy that does not run out, however it is a much more expensive that term life insurance policy

Uk Mortgage Life Insurance

Some funeral homes will certainly accept the project of a last expenditure life insurance policy and some will not. Some funeral homes require payment in advance and will certainly not wait until the last cost life insurance policy policy pays. It is best to take this into factor to consider when dealing when considering a final expense in.

You have several alternatives when it comes to purchasing home loan defense insurance policy. Among these, from our perspective and experience, we have located the adhering to business to be "the finest of the finest" when it comes to releasing home loan protection insurance coverage plans, and recommend any one of them if they are alternatives provided to you by your insurance policy representative or home mortgage lending institution.

Life Insurance To Cover Mortgage Payments

Can you obtain home loan protection insurance coverage for homes over $500,000? The largest distinction in between home loan defense insurance policy for homes over $500,000 and homes under $500,000 is the requirement of a clinical test.

Every firm is various, yet that is an excellent general rule. Keeping that stated, there are a few companies that offer home loan defense insurance approximately $1 million without any medical examinations. mortgage reducing term insurance. If you're home is worth less than $500,000, it's very most likely you'll get approved for plan that does not call for medical examinations

Mortgage protection for low earnings real estate usually isn't required as the majority of reduced income real estate systems are rented out and not possessed by the resident. The proprietor of the units can definitely purchase home mortgage protection for low income housing system renters if the plan is structured correctly. In order to do so, the property proprietor would certainly need to collaborate with an independent agent than can structure a group plan which permits them to combine the occupants on one policy.

If you have concerns, we highly suggest talking to Drew Gurley from Redbird Advisors. Drew Gurley is a participant of the Forbes Financing Council and has actually functioned several of the most distinct and varied home loan defense plans - mortgage insurance required. He can definitely help you think via what is needed to put this sort of plan together

Takes the uncertainty out of protecting your home if you pass away or come to be impaired. Money goes right to the mortgage company when a benefit is paid out.

{kind=link}

Latest Posts

Funeral Expense Plans

Final Expense Life Insurance Jobs

Burial Insurance State Farm